Financial Review

QUARTERLY STOCK PRICE INFORMATION, ISSUER PURCHASES OF EQUITY SECURITIES, DIVIDENDS, AND STOCK PERFORMANCE

Quarterly Stock Price Information

Our common stock is traded on the NASDAQ Stock Market under the symbol MSFT. On July 31, 2017, there were 101,825 registered holders of record of our common stock. The high and low common stock sales prices per share were as follows:

| Quarter Ended |

September 30 |

December 31 |

March 31 |

June 30 |

Fiscal Year |

| Fiscal Year 2017 |

| High |

$ 58.70 |

$ 64.10 |

$ 66.19 |

$ 72.89 |

$ 72.89 |

| Low |

$ 50.39 |

$ 56.32 |

$ 61.95 |

$ 64.85 |

$ 50.39 |

| Fiscal Year 2016 |

|

|

|

|

|

| High |

$ 48.41 |

$ 56.85 |

$ 55.64 |

$ 56.77 |

$ 56.85 |

| Low |

$ 39.72 |

$ 43.75 |

$ 48.19 |

$ 48.04 |

$ 39.72 |

SHARE REPURCHASES AND DIVIDENDS

Share Repurchases

On September 16, 2013, our Board of Directors approved a share repurchase program authorizing up to $40.0 billion in share repurchases. This share repurchase program became effective on October 1, 2013, and was completed on December 22, 2016.

On September 20, 2016, our Board of Directors approved a share repurchase program authorizing up to an additional $40.0 billion in share repurchases. This share repurchase program commenced on December 22, 2016 following completion of the prior program approved on September 16, 2013, has no expiration date, and may be suspended or discontinued at any time without notice. As of June 30, 2017, $36.8 billion remained of this $40.0 billion share repurchase program.

We repurchased the following shares of common stock under the share repurchase programs:

| (In millions) |

Shares |

|

Amount |

|

Shares |

|

Amount |

|

Shares |

|

Amount |

| Year Ended June 30, |

2017 |

2016 |

2015 |

| First Quarter |

63 |

|

$ 3,550 |

|

89 |

|

$ 4,000 |

|

43 |

|

$ 2,000 |

| Second Quarter |

59 |

|

3,533 |

|

66 |

|

3,600 |

|

43 |

|

2,000 |

| Third Quarter |

25 |

|

1,600 |

|

69 |

|

3,600 |

|

116 |

|

5,000 |

| Fourth Quarter |

23 |

|

1,600 |

|

70 |

|

3,600 |

|

93 |

|

4,209 |

| Total |

170 |

|

$ 10,283 |

|

294 |

|

$ 14,800 |

|

295 |

|

$ 13,209 |

Shares repurchased during the third and fourth quarter of fiscal year 2017 were under the share repurchase program approved September 20, 2016. All other shares repurchased were under the share repurchase program approved September 16, 2013. The above table excludes shares repurchased to settle statutory employee tax withholding related to the vesting of stock awards. All repurchases were made using cash resources.

Dividends

In fiscal year 2017, our Board of Directors declared the following dividends:

| Declaration Date |

Dividend

Per Share |

Record Date |

Total Amount |

Payment Date |

|

|

|

(In millions) |

|

| September 20, 2016 |

$ 0.39 |

November 17, 2016 |

$ 3,024 |

December 8, 2016 |

| November 30, 2016 |

0.39 |

February 16, 2017 |

3,012 |

March 9, 2017 |

| March 14, 2017 |

0.39 |

May 18, 2017 |

3,009 |

June 8, 2017 |

| June 13, 2017 |

0.39 |

August 17, 2017 |

3,006 |

September 14, 2017 |

The dividend declared on June 13, 2017 will be paid after the filing date of the 2017 Form 10-K and was included in other current liabilities as of June 30, 2017.

In fiscal year 2016, our Board of Directors declared the following dividends:

| Declaration Date |

Dividend

Per Share |

Record Date |

Total Amount |

Payment Date |

|

|

|

(In millions) |

|

| September 15, 2015 |

$ 0.36 |

November 19, 2015 |

$ 2,868 |

December 10, 2015 |

| December 2, 2015 |

0.36 |

February 18, 2016 |

2,842 |

March 10, 2016 |

| March 15, 2016 |

0.36 |

May 19, 2016 |

2,821 |

June 9, 2016 |

| June 14, 2016 |

0.36 |

August 18, 2016 |

2,800 |

September 8, 2016 |

The dividend declared on June 14, 2016 was included in other current liabilities as of June 30, 2016.

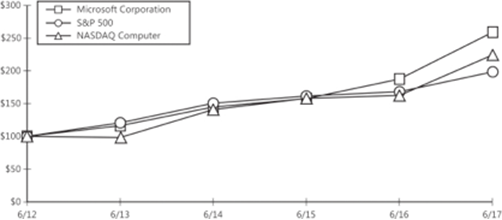

STOCK PERFORMANCE

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Microsoft Corporation, the S&P 500 Index, and the NASDAQ Computer Index

|

6/12 |

|

6/13 |

|

6/14 |

|

6/15 |

|

6/16 |

|

6/17 |

| Microsoft Corporation |

$ 100.00 |

|

$ 116.38 |

|

$ 144.62 |

|

$ 157.17 |

|

$ 187.22 |

|

$ 258.45 |

| S&P 500 |

100.00 |

|

120.60 |

|

150.27 |

|

161.43 |

|

167.87 |

|

197.92 |

| NASDAQ Computer |

100.00 |

|

98.40 |

|

140.53 |

|

157.83 |

|

162.37 |

|

223.98 |

- $100 invested on 6/30/12 in stock or index, including reinvestment of dividends.

Business

Note About Forward-Looking Statements

This report includes estimates, projections, statements relating to our business plans, objectives, and expected operating results that are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements may appear throughout this report, including the following sections: “Business,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties that may cause actual results to differ materially. We describe risks and uncertainties that could cause actual results and events to differ materially in “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and “Quantitative and Qualitative Disclosures about Market Risk” in our fiscal year 2017 Form 10-K. We undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events, or otherwise.

General

Our vision

Microsoft is a technology company whose mission is to empower every person and every organization on the planet to achieve more. We strive to create local opportunity, growth, and impact in every country around the world. Our strategy is to build best-in-class platforms and productivity services for an intelligent cloud and an intelligent edge infused with artificial intelligence (“AI”).

The way individuals and organizations use and interact with technology continues to evolve. A person’s experience with technology increasingly spans a multitude of devices and becomes more natural and multi-sensory with voice, ink, and gaze interactions. We believe a new technology paradigm is emerging that manifests itself through an intelligent cloud and an intelligent edge where computing is more distributed, AI drives insights and acts on the user’s behalf, and user experiences span devices with a user’s available data and information. We continue to transform our business to lead this new era of digital transformation and enable our customers and partners to thrive in this evolving world.

What we offer

Founded in 1975, we operate worldwide in over 190 countries. We develop, license, and support a wide range of software products, services, and devices that deliver new opportunities, greater convenience, and enhanced value to people’s lives. Our platforms and tools help drive small business productivity, large business competitiveness, and public-sector efficiency. They also support new startups, improve educational and health outcomes, and empower human ingenuity.

Our products include operating systems; cross-device productivity applications; server applications; business solution applications; desktop and server management tools; software development tools; video games; and training and certification of computer system integrators and developers. We also design, manufacture, and sell devices, including PCs, tablets, gaming and entertainment consoles, other intelligent devices, and related accessories, that integrate with our cloud-based offerings. We offer an array of services, including cloud-based solutions that provide customers with software, services, platforms, and content, and we provide solution support and consulting services. We also deliver relevant online advertising to a global audience.

The ambitions that drive us

To achieve our vision, our research and development efforts focus on three interconnected ambitions:

- Reinvent productivity and business processes.

- Build the intelligent cloud platform.

- Create more personal computing.

Reinvent productivity and business processes

We believe we can significantly enhance the lives of our customers using our broad portfolio of productivity, communication, and information products and services that span platforms and devices. Productivity is our first and foremost objective, to enable people to meet and collaborate more easily, and to effectively express ideas in new ways. We invent new scenarios that in turn create opportunity for our partners and help businesses accelerate their digital transformation while respecting each person’s privacy choices.

The foundation for these efforts rests on advancing our leading productivity, collaboration, communication, and business process tools including Microsoft Office, Microsoft Dynamics, and LinkedIn. With Office 365, we provide familiar industry-leading productivity and business process tools as cloud services, enabling access from anywhere and any device. New scenarios – like those enabled by Microsoft Teams – will redefine how work gets done and help foster employee engagement and culture. This work creates an opportunity to reach new customers and expand the usage of our services by our existing customers. We see opportunity in combining our offerings in new ways that are mobile, secure, collaborative, intelligent, and trustworthy. We offer our services across platforms and devices outside our own. As people move from device to device, so does their content and the richness of their services. We engineer our applications so users can find, try, and buy them in friction-free ways.

On December 8, 2016, we completed our acquisition of LinkedIn Corporation, the world’s largest professional network on the Internet. The acquisition is expected to accelerate the growth of Office 365, Dynamics 365, and LinkedIn.

Build the intelligent cloud platform

Cloud computing is foundational to enabling any organization’s digital transformation. In deploying technology that advances business strategy, enterprises decide what solutions will make employees more productive, collaborative, and satisfied, and connect with customers in new and compelling ways. Enterprises work to unlock business insights from a world of data. To achieve these objectives, they increasingly look to leverage the benefits of the cloud. Helping businesses digitally transform and move to the cloud is one of our largest opportunities. As one of the two largest providers of cloud computing at scale, we believe we work from a position of strength. The Microsoft Cloud is a secure solution that can listen, learn, and predict; turning data into actionable insight that enhances business opportunities. It provides a scalable and complete collaboration suite that transforms the way teams work. With the cloud, high-performance computing and agility can help businesses expand their growth.

Our cloud business benefits from three economies of scale: larger datacenters that deploy computational resources at significantly lower cost per unit than smaller ones; larger datacenters that coordinate and aggregate diverse customer, geographic, and application demand patterns, improving the utilization of computing, storage, and network resources; and multi-tenancy locations that lower application maintenance labor costs.

We believe our server products and cloud services, which include Microsoft SQL Server, Windows Server, Visual Studio, System Center, and Microsoft Azure, make us the only company with a public, private, and hybrid cloud platform that can power modern business. What differentiates Azure is our hybrid consistency, developer productivity, and software-as-a-service (“SaaS”) application integration. In addition, our hybrid infrastructure spans identity, data, compute, management, and security, helping to support the real-world needs and evolving regulatory requirements of commercial customers and enterprise-focused SaaS partners. We are working to enhance the customer’s return on investment by enabling enterprises to combine their existing datacenters and our public cloud into a single cohesive infrastructure. Businesses can deploy applications in their own datacenter, a partner’s datacenter, or in our datacenters with common security, management, and administration across all environments, providing the flexibility and scale they want. AI will be pervasive across devices, applications, and infrastructure to drive insights and act on the user’s behalf. Azure is also unique in its support for emerging applications so that Internet of Things (“IoT”) devices can act locally at the edge while taking advantage of the cloud for global coordination and machine learning at scale.

We enable organizations to securely adopt SaaS applications, both our own and third-party, and integrate them with their existing security and management infrastructure. We continue to innovate with higher-level services including identity and directory services that manage employee corporate identity and manage and secure corporate information accessed and stored across a growing number of devices, rich data storage and analytics services, machine learning services, media services, web and mobile backend services, and developer productivity services. To foster a rich developer ecosystem, our platform is extensible, enabling customers and partners to further customize and enhance our solutions, achieving even more value. This strategy requires continuing investment in datacenters and other infrastructure to support our services.

Create more personal computing

We strive to make computing more personal by putting users at the core of the experience, enabling them to interact with technology in more intuitive, engaging, and dynamic ways. Windows 10 is the cornerstone of our ambition to create more personal computing, allowing us to move from an operating system that runs on a PC to a service that can power the full spectrum of devices. Windows 10 is more personal and productive with functionality such as Cortana, Windows Hello, Windows Ink, Microsoft Edge, and universal applications. Windows 10 offers a foundation for the secure, modern workplace. Windows 10 is designed to foster innovation – from us, our partners, and developers – through rich and consistent experiences across the range of existing devices and entirely new device categories.

Our ambition for Windows 10 is to broaden our economic opportunity through three key levers: an original equipment manufacturer (“OEM”) ecosystem that creates exciting new hardware designs for Windows 10; our own commitment to the health and profitability of our first-party premium device portfolio; and monetization opportunities such as services, subscriptions, gaming, and search advertising. Our OEM partners are investing in an extensive portfolio of hardware designs and configurations for Windows 10. We now have the widest range of Windows hardware ever available.

With the unified Windows operating system, developers and OEMs can contribute to a thriving Windows ecosystem. We invest heavily to make Windows the most secure, manageable, and capable operating system for the needs of a modern workforce. We are working to create a broad developer opportunity by unifying the Windows installed base on Windows 10, and by enabling universal Windows applications to run across all device targets.

As part of our strategic objectives, we are committed to designing and marketing first-party devices to help drive innovation, create new categories, and stimulate demand in the Windows ecosystem. We are developing new input and output methods within Windows 10, including speech, pen, gesture, and mixed reality capabilities to power more personal computing experiences. The experiences and tools we build will unlock the creator in everyone and enable seamless teamwork not just in the workplace, but also at school and at home across all the devices people use.

Our future opportunity

Customers are looking to Microsoft and our thriving partner ecosystem to accelerate their own digital transformations and to unlock new opportunity in this era of intelligent cloud and intelligent edge. We continue to develop complete, intelligent solutions for our customers, including offerings like the recently introduced Microsoft 365 which brings together Office 365, Windows 10, and Enterprise Mobility and Security, that empower users to be creative and work together while safeguarding businesses and simplifying IT management. Our goal is to lead the industry in several distinct areas of technology over the long-term, which we expect will translate to sustained growth. We are investing significant resources in:

- Transforming the workplace to deliver new modular business applications to improve how people communicate, collaborate, learn, work, play, and interact with one another.

- Building and running cloud-based services in ways that unleash new experiences and opportunities for businesses and individuals, including converting data into AI.

- Using Windows to develop new categories of devices – both our own and third-party – as a person’s experience with technology becomes more natural, personal, and predictive with multi-sensory breakthroughs in voice, ink, gaze interactions, and augmented reality holograms.

- Inventing new gaming experiences that bring people together around their shared love for games, using an approach that enables people to play the games they want, with the people they want, on the devices they want.

- Applying AI to drive insights and act on our customer’s behalf by understanding and interpreting their needs using natural methods of communication.

Our future growth depends on our ability to transcend current product category definitions, business models, and sales motions. We have the opportunity to redefine what customers and partners can expect and are working to deliver new solutions that reflect the best of Microsoft.

OPERATING SEGMENTS

We operate our business and report our financial performance using three segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. Our segments provide management with a comprehensive financial view of our key businesses. The segments enable the alignment of strategies and objectives across the development, sales, marketing, and services organizations, and they provide a framework for timely and rational allocation of resources within businesses.

Additional information on our operating segments and geographic and product information is contained in Note 21 – Segment Information and Geographic Data of the Notes to Financial Statements.

Our reportable segments are described below.

Productivity and Business Processes

Our Productivity and Business Processes segment consists of products and services in our portfolio of productivity, communication, and information services, spanning a variety of devices and platforms. This segment primarily comprises:

- Office Commercial, including Office 365 subscriptions and Office licensed on-premises, comprising Office, Exchange, SharePoint, Skype for Business, and Microsoft Teams, and related Client Access Licenses (“CALs”).

- Office Consumer, including Office 365 subscriptions and Office licensed on-premises, and Office Consumer Services, including Skype, Outlook.com, and OneDrive.

- LinkedIn, including Talent Solutions, Marketing Solutions, and Premium Subscriptions.

- Dynamics business solutions, including Dynamics ERP on-premises, Dynamics CRM on-premises, and Dynamics 365, a set of cloud-based applications across ERP and CRM.

Office Commercial

Office Commercial is designed to increase personal, team, and organizational productivity through a range of products and services. Growth depends on our ability to reach new users, add value to our core product set, and continue to expand our product and service offerings into new markets such as security, analytics, collaboration, unified communications, and business intelligence. Office Commercial revenue is mainly affected by a combination of the demand from commercial customers for volume licensing, including Software Assurance, and the number of information workers in an enterprise, as well as the continued shift to Office 365. CALs provide certain Office Commercial products and services with access rights to our server products and CAL revenue is reported with the associated Office products and services.

Office Consumer

Office Consumer is designed to increase personal productivity through a range of products and services. Growth depends on our ability to reach new users, add value to our core product set, and continue to expand our product and service offerings into new markets. Office Consumer revenue is mainly affected by the percentage of customers that buy Office with their new devices and the continued shift to Office 365. Office Consumer Services revenue is mainly affected by the demand for communication and storage through Skype, Outlook.com, and OneDrive, which is largely driven by subscriptions, advertising, and the sale of minutes.

LinkedIn

LinkedIn connects the world’s professionals to make them more productive and successful, and is the world’s largest professional network on the Internet. LinkedIn offers services that can be used by customers to transform the way they hire, market, sell, and learn. In addition to LinkedIn’s free services, LinkedIn offers three categories of monetized solutions: Talent Solutions, Marketing Solutions, and Premium Subscriptions, which includes Sales Solutions. Talent Solutions is comprised of two elements: Hiring, and Learning and Development. Hiring provides services to recruiters that enable them to attract, recruit, and hire talent. Learning and Development provides subscriptions to enterprises and individuals to access online learning content. Marketing Solutions enables companies to advertise to LinkedIn’s member base. Premium Subscriptions enables professionals to manage their professional identity, grow their network, and connect with talent through additional services like premium search. Premium Subscriptions also includes Sales Solutions, which helps sales professionals find, qualify, and create sales opportunities and accelerate social selling capabilities. Growth will depend on our ability to increase the number of LinkedIn members and our ability to continue offering services that provide value for our members and increase their engagement. LinkedIn revenue is mainly affected by demand from enterprises and professional organizations for subscriptions to Talent Solutions and Premium Subscriptions offerings, as well as member engagement and the quality of the sponsored content delivered to those members to drive Marketing Solutions.

Dynamics

Dynamics provides on-premises and cloud-based business solutions for financial management, enterprise resource planning (“ERP”), customer relationship management (“CRM”), supply chain management, and analytics applications for small and medium businesses, large organizations, and divisions of global enterprises. Dynamics revenue is largely driven by the number of information workers licensed and the continued shift to Dynamics 365, a unified set of cloud-based intelligent business applications for enterprises.

Competition

Competitors to Office include software and global application vendors such as Adobe Systems, Apple, Cisco Systems, Facebook, Google, IBM, Oracle, SAP, and numerous web-based and mobile application competitors as well as local application developers in Asia and Europe. Cisco Systems is using its position in enterprise communications equipment to grow its unified communications business. Google provides a hosted messaging and productivity suite. Apple distributes versions of its pre-installed application software, such as email and calendar products, through its PCs, tablets, and phones. Skype for Business and Skype also compete with a variety of instant messaging, voice, and video communication providers, ranging from start-ups to established enterprises. Web-based offerings competing with individual applications have also positioned themselves as alternatives to our products. We believe our products compete effectively based on our strategy of providing powerful, flexible, secure, and easy-to-use solutions that work well with technologies our customers already have and are available on a device or via the cloud.

LinkedIn faces competition from online recruiting companies, talent management companies, and larger companies that are focusing on talent management and human resource services; job boards; traditional recruiting firms; and companies that provide learning and development products and services. Marketing Solutions competes with online and offline outlets that generate revenue from advertisers and marketers.

Dynamics competes with vendors such as Oracle and SAP in the market that provides solutions for large organizations and divisions of global enterprises. In the market that provides solutions for small and mid-sized businesses, our Dynamics products compete with vendors such as Infor, The Sage Group, and NetSuite. Salesforce.com’s cloud CRM offerings compete with our Dynamics CRM on-premises and Dynamics 365 offerings.

Intelligent Cloud

Our Intelligent Cloud segment consists of our public, private, and hybrid server products and cloud services that can power modern business. This segment primarily comprises:

- Server products and cloud services, including Microsoft SQL Server, Windows Server, Visual Studio, System Center, and related CALs, and Azure.

- Enterprise Services, including Premier Support Services and Microsoft Consulting Services.

Server Products and Cloud Services

Our server products are designed to make IT professionals, developers, and their systems more productive and efficient. Server software is integrated server infrastructure and middleware designed to support software applications built on the Windows Server operating system. This includes the server platform, database, business intelligence, storage, management and operations, virtualization, service-oriented architecture platform, security, and identity software. We also license standalone and software development lifecycle tools for software architects, developers, testers, and project managers. Server products and cloud services revenue is mainly affected by purchases through volume licensing programs, licenses sold to OEMs, and retail packaged products. CALs provide access rights to certain server products, including SQL Server and Windows Server, and revenue is reported along with the associated server product.

Azure is a scalable cloud platform with computing, networking, storage, database, and management, along with advanced services such as analytics, and comprehensive solutions such as Enterprise Mobility Suite. Azure includes a flexible platform that helps developers build, deploy, and manage enterprise, mobile, web, and IoT applications, for any platform or device without having to worry about the underlying infrastructure. Azure enables customers to devote more resources to development and use of applications that benefit their organizations, rather than managing on-premises hardware and software.

Enterprise Services

Enterprise Services, including Premier Support Services and Microsoft Consulting Services, assist customers in developing, deploying, and managing Microsoft server and desktop solutions and provide training and certification to developers and IT professionals on various Microsoft products.

Competition

Our server products face competition from a wide variety of server operating systems and applications offered by companies with a range of market approaches. Vertically integrated computer manufacturers such as Hewlett-Packard, IBM, and Oracle offer their own versions of the Unix operating system preinstalled on server hardware. Nearly all computer manufacturers offer server hardware for the Linux operating system and many contribute to Linux operating system development. The competitive position of Linux has also benefited from the large number of compatible applications now produced by many commercial and non-commercial software developers. A number of companies, such as Red Hat, supply versions of Linux.

We compete to provide enterprise-wide computing solutions and point solutions with numerous commercial software vendors that offer solutions and middleware technology platforms, software applications for connectivity (both Internet and intranet), security, hosting, database, and e-business servers. IBM and Oracle lead a group of companies focused on the Java Platform Enterprise Edition that competes with our enterprise-wide computing solutions. Commercial competitors for our server applications for PC-based distributed client-server environments include CA Technologies, IBM, and Oracle. Our web application platform software competes with open source software such as Apache, Linux, MySQL, and PHP. In middleware, we compete against Java vendors.

Our database, business intelligence, and data warehousing solutions offerings compete with products from IBM, Oracle, SAP, and other companies. Our system management solutions compete with server management and server virtualization platform providers, such as BMC, CA Technologies, Hewlett-Packard, IBM, and VMware. Our products for software developers compete against offerings from Adobe, IBM, Oracle, and other companies, and also against open-source projects, including Eclipse (sponsored by CA Technologies, IBM, Oracle, and SAP), PHP, and Ruby on Rails.

We believe our server products provide customers with advantages in performance, total costs of ownership, and productivity by delivering superior applications, development tools, compatibility with a broad base of hardware and software applications, security, and manageability.

Azure faces diverse competition from companies such as Amazon, Google, IBM, Oracle, Salesforce.com, VMware, and open source offerings. Azure’s competitive advantage includes enabling a hybrid cloud, allowing deployment of existing datacenters with our public cloud into a single, cohesive infrastructure, and the ability to run at a scale that meets the needs of businesses of all sizes and complexities.

Our Enterprise Services business competes with a wide range of companies that provide strategy and business planning, application development, and infrastructure services, including multinational consulting firms and small niche businesses focused on specific technologies.

More Personal Computing

Our More Personal Computing segment consists of products and services geared towards harmonizing the interests of end users, developers, and IT professionals across all devices. This segment primarily comprises:

- Windows, including Windows OEM licensing (“Windows OEM”) and other non-volume licensing of the Windows operating system; Windows Commercial, comprising volume licensing of the Windows operating system, Windows cloud services, and other Windows commercial offerings; patent licensing; Windows IoT; and MSN display advertising.

- Devices, including Microsoft Surface, PC accessories, and other intelligent devices.

- Gaming, including Xbox hardware and Xbox software and services, comprising Xbox Live transactions, subscriptions, and advertising (“Xbox Live”), video games, and third-party video game royalties.

- Search advertising.

Windows

The Windows operating system is designed to deliver a more personal computing experience for users by enabling consistency of experience, applications, and information across their devices. Windows OEM revenue is impacted significantly by the number of Windows operating system licenses purchased by OEMs, which they pre-install on the devices they sell. In addition to computing device market volume, Windows OEM revenue is impacted by:

- The mix of computing devices based on form factor and screen size.

- Differences in device market demand between developed markets and emerging markets.

- Attachment of Windows to devices shipped.

- Customer mix between consumer, small and medium businesses, and large enterprises.

- Changes in inventory levels in the OEM channel.

- Pricing changes and promotions, pricing variation that occurs when the mix of devices manufactured shifts from local and regional system builders to large multinational OEMs, and different pricing of Windows versions licensed.

- Piracy.

Windows Commercial revenue, which includes volume licensing of the Windows operating system, is affected mainly by the demand from commercial customers for volume licensing and Software Assurance, often reflecting the number of information workers in a licensed enterprise, and is therefore relatively independent of the number of PCs sold in a given year. Revenue from Windows cloud services, such as Windows Defender Advanced Threat Protection, and other Windows commercial offerings, is mainly impacted by attachment of Windows to devices shipped, pricing changes and promotions, mix of computing devices, and the customer mix among large enterprises, small and medium businesses, and educational institutions.

Patent licensing includes our programs to license patents we own for use across a broad array of technology areas, including mobile devices and cloud offerings.

Windows IoT extends the power of Windows and the cloud to intelligent systems by delivering specialized operating systems, tools, and services for use in embedded devices.

Display advertising primarily includes MSN ads. In June 2015, we entered into agreements with AOL and AppNexus to outsource our display sales responsibility.

Devices

We design, manufacture, and sell devices, including Surface, PC accessories, and other intelligent devices, such as Surface Hub and HoloLens. Our devices are designed to enable people and organizations to connect to the people and content that matter most using Windows and integrated Microsoft products and services. Surface is designed to help organizations, students, and consumers be more productive. We released the Surface Studio in December 2016 and our latest Surface devices, the Surface Laptop and Surface Pro, in June 2017.

In July 2015, we announced a plan to restructure our phone business to better focus and align resources. In May 2016, we announced plans to further streamline our smartphone hardware business. In November 2016, we completed the sale of our feature phone business.

Gaming

Our gaming platform is designed to provide a unique variety of entertainment using our devices, peripherals, applications, online services, and content. We released Xbox One and Xbox One S in November 2013 and August 2016, respectively, and announced Xbox One X in June 2017. With the launch of the Windows 10 Xbox app in July 2015, and the launch of the Mixer service in May 2017, we continue to open new opportunities for customers to engage both on- and off-console. Xbox Live enables people to connect and share online gaming experiences and is accessible on Xbox consoles, Windows-enabled devices, and other devices. Xbox Live is designed to benefit users by providing access to a network of certified applications and services and to benefit our developer and partner ecosystems by providing access to a large customer base. Xbox Live revenue is mainly affected by subscriptions and sales of Xbox Live enabled content, as well as advertising. We also design and sell gaming content to showcase our unique platform capabilities for Xbox consoles, Windows-enabled devices, and other devices. Growth of our gaming business is determined by the overall active user base through Xbox Live enabled content, availability of games, providing exclusive game content that gamers seek, the computational power and reliability of the devices used to access our content and services, and the ability to create new experiences via online services, downloadable content, and peripherals.

Search Advertising

Search advertising, including Bing and Bing Ads, is designed to deliver relevant online advertising to a global audience. We have several partnerships with other companies, including Oath (formerly Yahoo! and AOL) which is owned by Verizon, through which we provide and monetize search queries. Growth depends on our ability to attract new users, understand intent, and match intent with relevant content and advertiser offerings.

Competition

Windows faces competition from various software products and from alternative platforms and devices, mainly from Apple and Google. We believe Windows competes effectively by giving customers choice, value, flexibility, security, an easy-to-use interface, and compatibility with a broad range of hardware and software applications, including those that enable productivity.

Devices face competition from various computer, tablet, hardware, and phone manufacturers who offer a unique combination of high-quality industrial design and innovative technologies across various price points. These manufacturers, many of which are also current or potential partners and customers, include Apple and our Windows OEMs.

Our gaming platform competes with console platforms from Sony and Nintendo, both of which have a large, established base of customers. The lifecycle for gaming and entertainment consoles averages five to ten years. Nintendo released its latest generation console in March 2017 and Sony released its latest generation console in November 2013. We also compete with other providers of entertainment services through online marketplaces. We believe our gaming platform is effectively positioned against competitive products and services based on significant innovation in hardware architecture, user interface, developer tools, online gaming and entertainment services, and continued strong exclusive content from our own game franchises as well as other digital content offerings. Our video games competitors include Electronic Arts and Activision Blizzard. Xbox Live faces competition from various online marketplaces, including those operated by Amazon, Apple, and Google.

Our search advertising business competes with Google and a wide array of websites, social platforms like Facebook, and portals that provide content and online offerings to end users.

OPERATIONS

We have operations centers that support operations in their regions, including customer contract and order processing, credit and collections, information processing, and vendor management and logistics. The regional center in Ireland supports the European, Middle Eastern, and African region; the center in Singapore supports the Japan, India, Greater China, and Asia-Pacific region; and the centers in Fargo, North Dakota, Fort Lauderdale, Florida, Puerto Rico, Redmond, Washington, and Reno, Nevada support Latin America and North America. In addition to the operations centers, we also operate datacenters throughout the Americas, Australia, Europe, and Asia.

To serve the needs of customers around the world and to improve the quality and usability of products in international markets, we localize many of our products to reflect local languages and conventions. Localizing a product may require modifying the user interface, altering dialog boxes, and translating text.

Our devices are primarily manufactured by third-party contract manufacturers. We generally have the ability to use other manufacturers if a current vendor becomes unavailable or unable to meet our requirements.

We sold our feature phone business in November 2016, which included the sale of our phone manufacturing facility in Vietnam.

RESEARCH AND DEVELOPMENT

During fiscal years 2017, 2016, and 2015, research and development expense was $13.0 billion, $12.0 billion, and $12.0 billion, respectively. These amounts represented 14%, 14%, and 13% of revenue in fiscal years 2017, 2016, and 2015, respectively. We plan to continue to make significant investments in a broad range of research and development efforts.

Product and Service Development, and Intellectual Property

We develop most of our products and services internally through the following engineering groups.

- Office Product Group, focuses on our business across productivity, communications, education, and other information applications and services.

- Artificial Intelligence and Research, focuses on our AI development and other forward-looking research and development efforts spanning infrastructure, services, applications, and search.

- Cloud and Enterprise, focuses on our cloud infrastructure, server, database, CRM, ERP, management and development tools, and other business process applications and services for enterprises.

- Windows and Devices Group, focuses on our Windows platform, applications, games, store, and devices that power the Windows ecosystem.

- LinkedIn, focuses on our services that transform the way customers hire, market, sell, and learn.

Internal development allows us to maintain competitive advantages that come from product differentiation and closer technical control over our products and services. It also gives us the freedom to decide which modifications and enhancements are most important and when they should be implemented. We strive to obtain information as early as possible about changing usage patterns and hardware advances that may affect software design. Before releasing new software platforms, we provide application vendors with a range of resources and guidelines for development, training, and testing. Generally, we also create product documentation internally.

We protect our intellectual property investments in a variety of ways. We work actively in the U.S. and internationally to ensure the enforcement of copyright, trademark, trade secret, and other protections that apply to our software and hardware products, services, business plans, and branding. We are a leader among technology companies in pursuing patents and currently have a portfolio of over 66,000 U.S. and international patents issued and over 35,000 pending. While we employ much of our internally developed intellectual property exclusively in our products and services, we also engage in outbound and inbound licensing of specific patented technologies that are incorporated into licensees’ or Microsoft’s products. From time to time, we enter into broader cross-license agreements with other technology companies covering entire groups of patents. We also purchase or license technology that we incorporate into our products and services. At times, we make select intellectual property broadly available at no or low cost to achieve a strategic objective, such as promoting industry standards, advancing interoperability, or attracting and enabling our external development community.

While it may be necessary in the future to seek or renew licenses relating to various aspects of our products, services, and business methods, we believe, based upon past experience and industry practice, such licenses generally can be obtained on commercially reasonable terms. We believe our continuing research and product development are not materially dependent on any single license or other agreement with a third party relating to the development of our products.

Investing in the Future

Our success is based on our ability to create new and compelling products, services, and experiences for our users, to initiate and embrace disruptive technology trends, to enter new geographic and product markets, and to drive broad adoption of our products and services. We invest in a range of emerging technology trends and breakthroughs that we believe offer significant opportunities to deliver value to our customers and growth for the company. Based on our assessment of key technology trends, we maintain our long-term commitment to research and development across a wide spectrum of technologies, tools, and platforms spanning digital work and life experiences, cloud computing, AI, and hardware operating systems.

While our main research and development facilities are located in Redmond, Washington, we also operate research and development facilities in other parts of the U.S. and around the world, including Canada, China, India, Ireland, Israel, and the United Kingdom. This global approach helps us remain competitive in local markets and enables us to continue to attract top talent from across the world. We generally fund research at the corporate level to ensure that we are looking beyond immediate product considerations to opportunities further in the future. We also fund research and development activities at the operating segment level. Much of our segment level research and development is coordinated with other segments and leveraged across the company.

In addition to our main research and development operations, we also operate Microsoft Research. Microsoft Research is one of the world’s largest computer science research organizations, and works in close collaboration with top universities around the world to advance the state-of-the-art in computer science, providing us a unique perspective on future technology trends and contributing to our innovation.

DISTRIBUTION, SALES, AND MARKETING

We market and distribute our products and services through the following channels: OEMs, direct, and distributors and resellers. Our sales force performs a variety of functions, including working directly with enterprises and public-sector organizations worldwide to identify and meet their technology requirements; managing OEM relationships; and supporting system integrators, independent software vendors, and other partners who engage directly with our customers to perform sales, consulting, and fulfillment functions for our products and services.

OEMs

We distribute our software through OEMs that pre-install our software on new devices and servers they sell. The largest component of the OEM business is the Windows operating system pre-installed on devices. OEMs also sell devices pre-installed with other Microsoft products and services, including applications such as Office and the capability to subscribe to Office 365.

There are two broad categories of OEMs. The largest category of OEMs are direct OEMs as our relationship with them is managed through a direct agreement between Microsoft and the OEM. We have distribution agreements covering one or more of our products with virtually all the multinational OEMs, including Acer, ASUS, Dell, Fujitsu, Hewlett-Packard, Lenovo, Samsung, Toshiba, and with many regional and local OEMs. The second broad category of OEMs are system builders consisting of lower-volume PC manufacturers, which source Microsoft software for pre-installation and local redistribution primarily through the Microsoft distributor channel rather than through a direct agreement or relationship with Microsoft.

Direct

Many organizations that license our products and services transact directly with us through Enterprise Agreements and Enterprise Services contracts, with sales support from system integrators, independent software vendors, web agencies, and partners that advise organizations on licensing our products and services (“Enterprise Agreement Software Advisors”, or “ESA”). Microsoft offers direct sales programs targeted to reach small, medium, and corporate customers, in addition to those offered through the reseller channel. A large network of partner advisors support many of these sales.

We also provide commercial and consumer products and services directly to customers, such as cloud services, search, and gaming, through our online portals, marketplaces, and retail stores.

Distributors and Resellers

Organizations also license our products and services indirectly, primarily through licensing solution partners (“LSP”), distributors, value-added resellers (“VAR”), OEMs, and retailers. Although each type of reselling partner may reach organizations of all sizes, LSPs are primarily engaged with large organizations, distributors resell primarily to VARs, and VARs typically reach small and medium organizations. ESAs are also typically authorized as LSPs and operate as resellers for our other volume licensing programs. Microsoft Cloud Solution Provider is our main partner program for reselling cloud services.

Our Dynamics software offerings are also licensed to enterprises through a global network of channel partners providing vertical solutions and specialized services. We distribute our retail packaged products primarily through independent non-exclusive distributors, authorized replicators, resellers, and retail outlets. Individual consumers obtain these products primarily through retail outlets. We distribute our devices through third-party retailers. We have a network of field sales representatives and field support personnel that solicit orders from distributors and resellers, and provide product training and sales support.

LICENSING OPTIONS

We offer options for organizations that want to purchase our cloud services, on-premises software, and Software Assurance. We license software to organizations under volume licensing agreements to allow the customer to acquire multiple licenses of products and services instead of having to acquire separate licenses through retail channels. We use different programs designed to provide flexibility for organizations of various sizes. While these programs may differ in various parts of the world, generally they include those discussed below.

Software Assurance conveys rights to new software and upgrades for perpetual licenses released over the contract period. It also provides support, tools, and training to help customers deploy and use software efficiently. Software Assurance is included with certain volume licensing agreements and is an optional purchase with others.

Volume Licensing Programs

Enterprise Agreement

Enterprise Agreements offer large organizations a manageable volume licensing program that gives them the flexibility to buy cloud services and software licenses under one agreement. Enterprise Agreements are designed for medium or large organizations that want to license cloud services and on-premises software organization-wide over a three-year period. Organizations can elect to purchase perpetual licenses or subscribe to licenses. Software Assurance is included.

Microsoft Product and Services Agreement

MPSAs are designed for medium and large organizations that want to license cloud services and on-premises software as needed, with no organization-wide commitment, under a single, non-expiring agreement. Organizations purchase perpetual licenses or subscribe to licenses. Software Assurance is optional for customers that purchase perpetual licenses.

Open

Open Licensing agreements are a simple, cost-effective way to acquire the latest Microsoft technology. Open Licensing agreements are designed for small and medium organizations that want to license cloud services and on-premises software over a one- to three-year period. Under the Open License program, organizations purchase perpetual licenses and Software Assurance is optional. Under Open Value programs, organizations can elect to purchase perpetual licenses or subscribe to licenses and Software Assurance is included.

Select Plus

Select Plus agreements are designed for government and academic organizations to acquire on-premises licenses at any affiliate or department level, while realizing advantages as one organization. Organizations purchase perpetual licenses and Software Assurance is optional.

In July 2014, we announced the retirement over a two-year period of Select Plus agreements for commercial organizations. Beginning July 2015, no new Select Plus agreements were signed with commercial organizations. Starting in July 2016, we no longer accept orders from commercial organizations for Select Plus after their next agreement anniversary.

Microsoft Online Subscription Agreement

Microsoft Online Subscription Agreement is designed for small and medium organizations that want to subscribe to, activate, provision, and maintain cloud services seamlessly and directly via the web, through the Microsoft Online Subscription Program. The program allows customers to acquire monthly or annual subscriptions for cloud-based services.

Partner Programs

The Microsoft Cloud Solution Provider program offers customers an easy way to license the cloud services they need in combination with the value-added services offered by their systems integrator, hosting partner, or cloud reseller partner. Partners in this program can easily package their own products and services to directly provision, manage, and support their customer subscriptions.

The Microsoft Services Provider License Agreement allows service providers and independent software vendors who want to license eligible Microsoft software products to provide software services and hosted applications to their end customers. Partners license software over a three-year period and are billed monthly based on consumption.

The Independent Software Vendor Royalty program enables partners to integrate Microsoft products into other applications and then license the unified business solution to their end users.

CUSTOMERS

Our customers include individual consumers, small and medium organizations, large global enterprises, public-sector institutions, Internet service providers, application developers, and OEMs. No sales to an individual customer accounted for more than 10% of revenue in fiscal years 2017, 2016, or 2015. Our practice is to ship our products promptly upon receipt of purchase orders from customers; consequently, backlog is not significant.

EMPLOYEES

As of June 30, 2017, we employed approximately 124,000 people on a full-time basis, 73,000 in the U.S. and 51,000 internationally. Of the total employed people, 39,000 were in operations, including manufacturing, distribution, product support, and consulting services; 40,000 were in product research and development; 34,000 were in sales and marketing; and 11,000 were in general and administration. The acquisition of LinkedIn Corporation resulted in the addition of approximately 11,000 people in fiscal year 2017. Certain of our employees are subject to collective bargaining agreements.

AVAILABLE INFORMATION

Our Internet address is www.microsoft.com. At our Investor Relations website, www.microsoft.com/investor, we make available free of charge a variety of information for investors. Our goal is to maintain the Investor Relations website as a portal through which investors can easily find or navigate to pertinent information about us, including:

- Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, as soon as reasonably practicable after we electronically file that material with or furnish it to the Securities and Exchange Commission (“SEC”).

- Information on our business strategies, financial results, and metrics for investors.

- Announcements of investor conferences, speeches, and events at which our executives talk about our product, service, and competitive strategies. Archives of these events are also available.

- Press releases on quarterly earnings, product and service announcements, legal developments, and international news.

- Corporate governance information including our articles of incorporation, bylaws, governance guidelines, committee charters, codes of conduct and ethics, global corporate social responsibility initiatives, and other governance-related policies.

- Other news and announcements that we may post from time to time that investors might find useful or interesting.

- Opportunities to sign up for email alerts and RSS feeds to have information pushed in real time.

The information found on our website is not part of this or any other report we file with, or furnish to, the SEC. In addition to these channels, we use social media to communicate to the public. It is possible that the information we post on social media could be deemed to be material to investors. We encourage investors, the media, and others interested in Microsoft to review the information we post on the social media channels listed on our Investor Relations website.

Discussion & Analysis

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) is intended to help the reader understand the results of operations and financial condition of Microsoft Corporation. MD&A is provided as a supplement to, and should be read in conjunction with, our financial statements and the accompanying Notes to Financial Statements.

OVERVIEW

Microsoft is a technology company whose mission is to empower every person and every organization on the planet to achieve more. We strive to create local opportunity, growth, and impact in every country around the world. Our strategy is to build best-in-class platforms and productivity services for an intelligent cloud and an intelligent edge infused with artificial intelligence (“AI”). We develop, license, and support a wide range of software products, services, and devices that deliver new opportunities, greater convenience, and enhanced value to people’s lives. Our platforms and tools help drive small business productivity, large business competitiveness, and public-sector efficiency. They also support new startups, improve educational and health outcomes, and empower human ingenuity.

We generate revenue by licensing and supporting an array of software products, by offering a wide range of cloud-based and other services to consumers and businesses, by designing, manufacturing, and selling devices that integrate with our cloud-based services, and by delivering relevant online advertising to a global audience. Our most significant expenses are related to compensating employees; designing, manufacturing, marketing, and selling our products and services; datacenter costs in support of our cloud-based services; and income taxes.

Highlights* from fiscal year 2017 included:

- Commercial cloud annualized revenue run rate** exceeded $18.9 billion.

- Office Commercial revenue grew 6%, driven by Office 365 commercial revenue growth of 46%.

- Office Consumer revenue grew 14%, and Office 365 consumer subscribers increased to 27.0 million.

- Microsoft Dynamics revenue grew 9%, driven by Dynamics 365 revenue growth of 78%.

- LinkedIn contributed revenue of $2.3 billion.

- Server products and cloud services revenue grew 13%, driven by Microsoft Azure revenue growth of 99%.

- Enterprise Services revenue decreased 2%, driven by a decline in revenue from custom support agreements, offset in part by higher revenue from Premier Support Services and Microsoft Consulting Services.

- Windows original equipment manufacturer licensing (“Windows OEM”) revenue increased 3%.

- Windows Commercial revenue grew 5%, driven by multi-year agreement revenue.

- Microsoft Surface revenue decreased 2%, driven by a reduction in volumes sold, offset in part by a higher mix of premium devices.

- Search advertising revenue, excluding traffic acquisition costs, grew 9%.

- Gaming revenue decreased slightly, driven by lower Xbox hardware revenue, offset in part by growth in Xbox software and services.

- Highlights are presented based on segment results.

- Commercial cloud annualized revenue run rate is calculated by multiplying revenue for the last month of the quarter by twelve for Office 365 commercial, Azure, Dynamics 365, and other cloud properties.

On December 8, 2016, we completed our acquisition of LinkedIn Corporation for a total purchase price of $27.0 billion. LinkedIn has been included in our consolidated results of operations since the date of acquisition. See Note 9 – Business Combinations in the Notes to Financial Statements for further discussion.

In November 2016, we completed the sale of our feature phone business for $350 million.

In July 2015, we announced a plan to restructure our phone business to better focus and align resources. In May 2016, we announced plans to further streamline our smartphone hardware business. Our change in phone strategy resulted in a reduction in units sold and associated expenses in fiscal year 2016 and 2017.

Industry Trends

Our industry is dynamic and highly competitive, with frequent changes in both technologies and business models. Each industry shift is an opportunity to conceive new products, new technologies, or new ideas that can further transform the industry and our business. At Microsoft, we push the boundaries of what is possible through a broad range of research and development activities that seek to identify and address the changing demands of customers and users, industry trends, and competitive forces.

Economic Conditions, Challenges, and Risks

The markets for software, devices, and cloud-based services are dynamic and highly competitive. Our competitors are developing new software and devices, while also deploying competing cloud-based services for consumers and businesses. The devices and form factors customers prefer evolve rapidly, and influence how users access services in the cloud, and in some cases, the user’s choice of which suite of cloud-based services to use. We must continue to evolve and adapt over an extended time in pace with this changing environment. The investments we are making in infrastructure and devices will continue to increase our operating costs and may decrease our operating margins.

Our success is highly dependent on our ability to attract and retain qualified employees. We hire a mix of university and industry talent worldwide. Microsoft competes for talented individuals globally by offering an exceptional working environment, broad customer reach, scale in resources, the ability to grow one’s career across many different products and businesses, and competitive compensation and benefits. Aggregate demand for our software, services, and devices is correlated to global macroeconomic and geopolitical factors, which remain dynamic.

Our international operations provide a significant portion of our total revenue and expenses. Many of these revenue and expenses are denominated in currencies other than the U.S. dollar. As a result, changes in foreign exchange rates may significantly affect revenue and expenses. The strengthening of the U.S. dollar relative to certain foreign currencies throughout fiscal year 2015, 2016, and 2017, negatively impacted reported revenue and reduced reported expenses from our international operations.

See a discussion of these factors and other risks under Risk Factors in our fiscal year 2017 Form 10-K.

Seasonality

Our revenue historically has fluctuated quarterly and has generally been highest in the second quarter of our fiscal year due to corporate calendar year-end spending trends in our major markets and holiday season spending by consumers.

Reportable Segments

We report our financial performance based on the following segments: Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The segment amounts included in MD&A are presented on a basis consistent with our internal management reporting. All differences between our internal management reporting basis and accounting principles generally accepted in the United States (“U.S. GAAP”), along with certain corporate-level and other activity, are included in Corporate and Other. We have recast certain previously reported amounts to conform to the way we internally manage and monitor segment performance.

Additional information on our reportable segments is contained in Note 21 – Segment Information and Geographic Data of the Notes to Financial Statements.

SUMMARY RESULTS OF OPERATIONS

| (In millions, except percentages and per share amounts) |

2017 |

2016 |

2015 |

Percentage

Change 2017

Versus 2016 |

Percentage

Change 2016

Versus 2015 |

| Revenue |

$ 89,950 |

$ 85,320 |

$ 93,580 |

5% |

(9)% |

| Gross margin |

55,689 |

52,540 |

60,542 |

6% |

(13)% |

| Operating income |

22,326 |

20,182 |

18,161 |

11% |

11% |

| Diluted earnings per share |

2.71 |

2.10 |

1.48 |

29% |

42% |

Fiscal year 2017 compared with fiscal year 2016

Revenue increased $4.6 billion or 5%, driven by growth in Productivity and Business Processes and Intelligent Cloud, offset in part by lower revenue from More Personal Computing. Productivity and Business Processes revenue increased, driven by the acquisition of LinkedIn and higher revenue from Microsoft Office. Intelligent Cloud revenue increased, primarily due to higher revenue from server products and cloud services. More Personal Computing revenue decreased, mainly due to lower revenue from Devices, offset in part by higher revenue from Windows and Search advertising. Revenue included an unfavorable foreign currency impact of 2%.

Gross margin increased $3.1 billion or 6%, due to growth across each of our segments, including the acquisition of LinkedIn, driven by higher revenue. Gross margin included an unfavorable foreign currency impact of 2%. Gross margin percentage increased slightly due to a margin percent increase in More Personal Computing and segment sales mix, offset in part by margin percent declines in Productivity and Business Processes and Intelligent Cloud. Gross margin percentage includes a 5-point improvement in commercial cloud gross margin primarily across Azure and Office 365.

Operating income increased $2.1 billion or 11%, primarily due to higher gross margin and lower impairment, integration, and restructuring expenses, offset in part by an increase in research and development and sales and marketing expenses. Operating income included an operating loss of $948 million related to the acquisition of LinkedIn, including $866 million of amortization of intangible assets. Operating income also included an unfavorable foreign currency impact of 4%. Key changes in expenses were:

- Cost of revenue increased $1.5 billion or 5%, mainly due to growth in our commercial cloud, the acquisition of LinkedIn, and higher Search advertising traffic acquisition costs, offset in part by a reduction in phone sales and Gaming cost of revenue.

- Research and development expenses increased $1.0 billion or 9%, primarily due to LinkedIn expenses and increased investments in cloud engineering, offset in part by a reduction in phone expenses.

- Sales and marketing expenses increased $842 million or 6%, primarily due to LinkedIn expenses and increased investments in sales capacity for our commercial cloud, offset in part by a reduction in phone and marketing expenses.

- Impairment, integration, and restructuring expenses decreased $804 million, driven by prior year asset impairment charges and restructuring charges related to our phone business, offset in part by current year employee severance expenses primarily related to our sales and marketing restructuring plan.

Diluted earnings per share (“EPS”) was $2.71 for fiscal year 2017. Current year diluted EPS was negatively impacted by the net revenue deferral from Windows 10 and restructuring expenses, which resulted in a decrease in diluted EPS of $0.60. Diluted EPS was $2.10 for fiscal year 2016. Prior year diluted EPS was negatively impacted by the net revenue deferral from Windows 10 and impairment and restructuring expenses, which resulted in a decrease in diluted EPS of $0.69.

Fiscal year 2016 compared with fiscal year 2015

Revenue decreased $8.3 billion or 9%, primarily due to the impact of the net revenue deferral from Windows 10 of $6.6 billion and an unfavorable foreign currency impact of approximately $3.8 billion or 4%. Windows 10 revenue is primarily recognized at the time of billing in the More Personal Computing segment, and the deferral and subsequent recognition of revenue is reflected in Corporate and Other. More Personal Computing revenue decreased, mainly due to lower revenue from Devices and Windows, offset in part by higher revenue from Search advertising and Gaming. Intelligent Cloud revenue increased, primarily due to higher revenue from server products and cloud services and Enterprise Services. Productivity and Business Processes revenue increased slightly, driven by an increase in Office and Dynamics revenue.

Operating income increased $2.0 billion or 11%, primarily due to a decrease in impairment, integration, and restructuring expenses and sales and marketing expenses, offset in part by lower gross margin. Gross margin decreased $8.0 billion or 13%, driven by the decline in revenue as discussed above, and included an unfavorable foreign currency impact of approximately $3.3 billion or 5%. Productivity and Business Processes and More Personal Computing gross margin decreased, offset in part by higher gross margin from Intelligent Cloud.

Key changes in expenses were:

- Cost of revenue decreased $258 million or 1%, mainly due to a reduction in phone sales, driven by the change in strategy for the phone business, offset in part by growth in commercial cloud and Search advertising.

- Impairment, integration, and restructuring expenses decreased $8.9 billion, primarily driven by prior year goodwill and asset impairment charges related to our phone business and restructuring charges associated with our phone business restructuring plans.

- Sales and marketing expenses decreased $1.0 billion or 6%, driven by a reduction in phone expenses and a favorable foreign currency impact of approximately 2%.

Diluted EPS was $2.10 for fiscal year 2016. Diluted EPS was negatively impacted by the net revenue deferral from Windows 10 and impairment, integration, and restructuring expenses, which resulted in a decrease to diluted EPS of $0.69. Diluted EPS was $1.48 for fiscal year 2015. Diluted EPS was negatively impacted by impairment, integration, and restructuring expenses, which resulted in a decrease to diluted EPS of $1.15.

SEGMENT RESULTS OF OPERATIONS

| (In millions, except percentages) |

2017 |

|

2016 |

|

2015 |

Percentage

Change 2017

Versus 2016 |

Percentage

Change 2016

Versus 2015 |

| Revenue |

|

|

|

|

|

|

|

| Productivity and Business Processes |

$ 30,444 |

|

$ 26,487 |

|

$ 26,430 |

15% |

0% |

| Intelligent Cloud |

27,440 |

|

25,042 |

|

23,715 |

10% |

6% |

| More Personal Computing |

38,773 |

|

40,434 |

|

43,435 |

(4)% |

(7)% |

| Corporate and Other |

(6,707) |

|

(6,643) |

|

0 |

(1)% |

* |

| Total |

$ 89,950 |

|

$ 85,320 |

|

$ 93,580 |

5% |

(9)% |

|

| Operating income (loss) |

|

|

|

|

|

|

|

| Productivity and Business Processes |

$ 11,913 |

|

$ 12,418 |

|

$ 13,274 |

(4)% |

(6)% |

| Intelligent Cloud |

9,138 |

|

9,315 |

|

9,803 |

(2)% |

(5)% |

| More Personal Computing |

8,288 |

|

6,202 |

|

5,095 |

34% |

22% |

| Corporate and Other |

(7,013) |

|

(7,753) |

|

(10,011) |

* |

* |

| Total |

$ 22,326 |

|

$ 20,182 |

|

$ 18,161 |

11% |

11% |

- Not meaningful

Reportable Segments

Fiscal year 2017 compared with fiscal year 2016

Productivity and Business Processes

Revenue increased $4.0 billion or 15%, driven by the acquisition of LinkedIn and higher revenue from Office.

- LinkedIn revenue was $2.3 billion, primarily comprised of revenue from Talent Solutions.

- Office Commercial revenue increased $1.2 billion or 6%, driven by higher revenue from Office 365 commercial, mainly due to growth in subscribers, offset in part by lower revenue from products licensed on-premises, reflecting a continued shift to Office 365 commercial.

- Office Consumer revenue increased $425 million or 14%, driven by higher revenue from Office 365 consumer, mainly due to growth in subscribers.

- Dynamics revenue increased 9%, primarily due to higher revenue from Dynamics 365.

Operating income decreased $505 million or 4%, primarily due to higher operating expenses, offset in part by higher gross margin. Operating income included an unfavorable foreign currency impact of 3%.

- Operating expenses increased $2.4 billion or 26%, mainly due to LinkedIn and cloud engineering expenses. Operating expenses included $2.3 billion related to our acquisition of LinkedIn, including $359 million of amortization of acquired intangible assets. Sales and marketing expenses increased $1.2 billion or 24%, research and development expenses increased $955 million or 35%, and general and administrative expenses increased $212 million or 14%.

- Gross margin increased $1.8 billion or 9%, primarily due to our acquisition of LinkedIn. Gross margin percentage decreased due to an increased mix of cloud offerings and amortization of acquired intangible assets related to LinkedIn. Cost of revenue included $918 million related to our acquisition of LinkedIn, including $507 million of amortization of acquired intangible assets.

Intelligent Cloud

Revenue increased $2.4 billion or 10%, primarily due to higher revenue from server products and cloud services.

- Server products and cloud services revenue grew $2.5 billion or 13%, driven by Azure revenue growth of 99% and server products licensed on-premises revenue growth of 4%.

- Enterprise Services revenue decreased 2%, driven by a decline in revenue from custom support agreements, offset in part by higher revenue from Premier Support Services and Microsoft Consulting Services.

Operating income decreased $177 million or 2%, primarily due to higher operating expenses, offset in part by higher gross margin. Operating income included an unfavorable foreign currency impact of 3%.

- Operating expenses increased $973 million or 11%, driven by investments in sales capacity, cloud engineering, and developer engagement. Sales and marketing expenses increased $547 million or 13%, research and development expenses increased $468 million or 14%, and general and administrative expenses decreased $42 million or 3%.

- Gross margin increased $796 million or 4%, driven by growth in server products and cloud services revenue and cloud services scale and efficiencies, offset in part by a decline in Enterprise Services gross margin. Gross margin included an unfavorable foreign currency impact of 2%. Gross margin percentage decreased due to an increased mix of cloud offerings and lower Enterprise Services gross margin percent, offset by improvement in Azure gross margin percent.

More Personal Computing

Revenue decreased $1.7 billion or 4%, mainly due to lower revenue from Devices, offset in part by higher revenue from Windows and Search advertising.

- Windows revenue increased $442 million or 3%, mainly due to higher revenue from Windows OEM and Windows Commercial. Windows OEM revenue increased 3%. Windows OEM Pro revenue grew 5%, outperforming the commercial PC market, primarily due to a higher mix of premium licenses sold. Windows OEM non-Pro revenue grew 1%, outperforming the consumer PC market, primarily due to a higher mix of premium devices sold. Windows Commercial revenue grew 5%, driven by multi-year agreement revenue.

- Search advertising revenue increased $791 million or 15%. Search advertising revenue, excluding traffic acquisition costs, increased 9%, primarily driven by growth in Bing, due to higher revenue per search and search volume.

- Gaming revenue decreased slightly, primarily due to lower Xbox hardware revenue, offset in part by higher revenue from Xbox software and services. Xbox hardware revenue decreased 21%, mainly due to lower prices of consoles sold and a decline in volume of consoles sold. Xbox software and services revenue increased 11%, driven by a higher volume of Xbox Live transactions and revenue per transaction.

- Surface revenue decreased $82 million or 2%, primarily due to a reduction in volumes sold, offset in part by a higher mix of premium devices.

- Phone revenue decreased $2.8 billion.

Operating income increased $2.1 billion or 34%, due to lower operating expenses and higher gross margin. Operating income included an unfavorable foreign currency impact of 4%.