Top 10 digital strategies and technology trends for insurance executives

The insurance industry is facing a fast-changing landscape. As the world deals with COVID-19, insurers are seeing changing customer and employee expectations. This is in addition to the “cost-conscious” customer, who changes from one insurer to another. Now more than ever, insurance leaders are seeking digital transformation and innovation while reducing costs of operations.

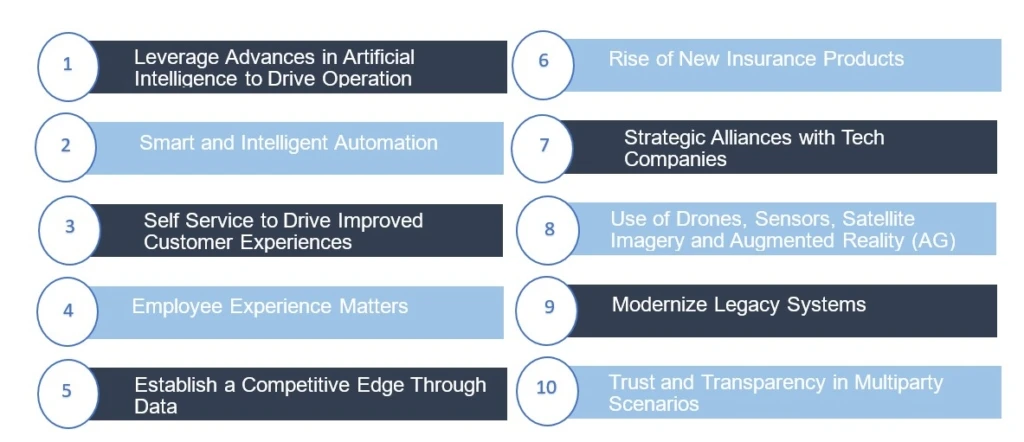

Here are 10 strategies that insurance professionals should consider when building their strategy:

Technology strategy 1: Leverage advances in Artificial Intelligence (AI) to drive operational improvement and new opportunities

There are three main areas of benefit from AI: detecting insurance fraud, reducing claim costs, and mining voice data to enhance customer service.

Natural Language Processing (NLP) allows unstructured documents, such as claim adjuster notes, to add even more value, serving as a mechanism to detect fraudulent claims and patterns of fraud. NLP can also be used to read and process handwritten insurance-related forms and mine information to save the insurer money on claim costs. Voice recordings from agents and customers can also be used to enhance the overall customer experience and improve service.

Technology strategy 2: Smart and intelligent automation

Smart and intelligent automation focuses on the application of advances in predictive analytics and Machine Learning, applied beyond automating data collection processes through the use of robotic process automation (RPA) tools. Insurers should explore automating processes like property assessment, personalized customer interactions, fraud detection, and claims processing and verification. There is a huge opportunity to redefine operational improvements in call centers with voice translation, automated call monitoring for sentiment analysis leading to early escalations. Insurers can also benefit from a virtual call center that does not have all agents in one location and some agents are remote.

Technology strategy 3: Self-service drives “improved experience” while lowering costs

The food and retail industry are large proponents of the use of self-service for improved customer experience. However, this can also greatly benefit insurance companies for similar reasons. Implementing self-service both in claim settlement (touchless claims with automated claims payouts) and customer care through bots and virtual agents can cut costs, increase customer satisfaction, and lead to more personalized customer experiences.

Technology strategy 4: Employee experience matters (without compromising security)

Most companies regularly invest in their brand and customer experiences, but many forget to invest in a crucial component of a successful company: the experiences of their employees. To attract, retain, and boost the productivity of employees, insurance companies should increasingly look for ways to improve employee experience—whether virtually or in person—without compromising on security. With COVID-19, we have all learned the value of social distancing and insurers are redesigning workspaces to better address employee health. With an increasing number of remote employees, the employee experience and need for productivity from any place and location will be even more important.

Technology strategy 5: Competitive edge through data

Insurance has always leveraged data and thrived on data analytics. However, the need for data is more important now more than ever. Pairing big data with machine learning and predictive analytics, companies can leverage data to bring about new products, save costs, and stay competitive. Insurers are reinventing underwriting by leveraging new sources of data for competitive advantage and offering new products.

Technology strategy 6: Rise of new insurance products

The increasing shift towards autonomous cars and the use of sensors and IoT creates a disruption for insurance companies. Companies need to shift focus and tackle new opportunities appearing alongside these new technologies. New insurance products will emerge, insuring new types of risk. Technology teams will need to be prepared to support these new products.

Technology strategy 7: More insurance companies will have strategic alliances with tech companies

The advances in big data, AI, and data analytics are causing insurance companies to become more technology and data-driven than ever. As technology adoption increases, insurers will need to improve their technical capability. To strengthen their technical capability, insurers will seek access to big tech partners and influence features in their technology to stay competitive. Already, a handful of leading insurers have formed strategic alliances.

Technology strategy 8: Use of drones, sensors, satellite imagery, and Augmented Reality (AR) and Virtual Reality (VR)

Many of the processes that are typically done in person, such as user and employee education, coverage decisions, and damage prevention are being simplified with technology, creating a more immersive, accurate, and cost-effective experience for insurance companies. The use of augmented and virtual reality applies to the claims handling process, accident recreation, and many more processes. Uses of other technology, such as smart sensors or satellites to prevent and assess damage or reduce costs, will continue to increase.

Technology strategy 9: Legacy system modernization

Many insurers are still running old technology that is due for an upgrade. The benefits range from a reduction in costs, business agility, and improved productivity and user experience. Being able to leverage the advancements in new technology and the various new FinTech offerings is also a key benefit of system modernization.

Technology strategy 10: Trust and transparency in multiparty scenarios

Leveraging technologies that lead to increased trust and transparency in the transaction will lead to cost savings. Some scenarios include digital subrogation (where the insurance company collects money from the party at fault or their insurance company), workers’ compensation with worker presence verification, and digital identity services. Some insurance companies are also exploring ways to make the premium breakup more transparent to the customer as a way to ensure loyalty.

To learn more about building strong business strategies and read how carriers have modernized operations and strengthened customers’ experiences, visit our customer stories portal.